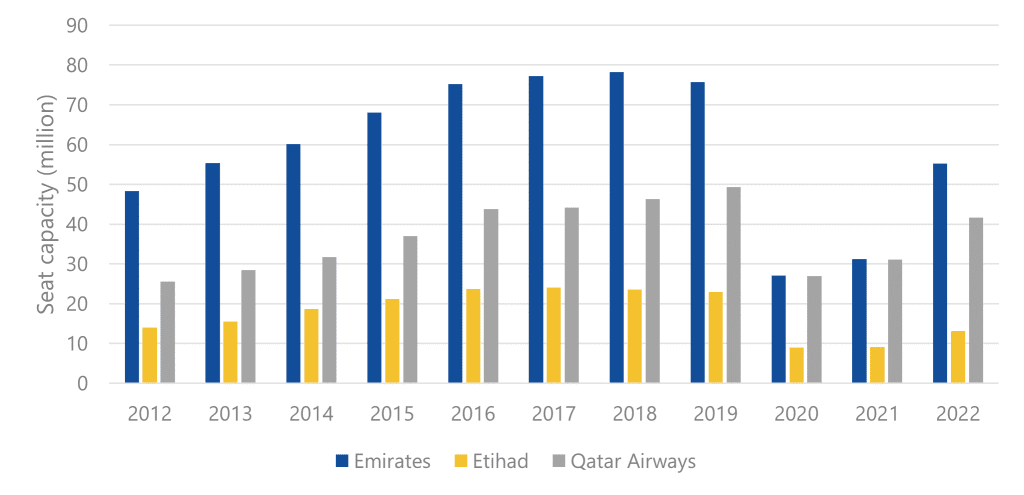

The triumvirate of leading Middle Eastern airlines – comprised of Emirates, Etihad and Qatar Airways and often referred to as the ME3 – is evolving into the ME2 with Etihad now pursuing a much more conservative path.

New Delhi, 20 July 2022: This strategic shift was visible even prior to COVID-19, with Etihad’s capacity plateauing since 2016. But it has become more pronounced in the aftermath of the pandemic as a result of Etihad’s relatively slower recovery and Qatar Airways’ continued expansion. Etihad and its hub at Abu Dhabi have moderated their ambitions in recent years as a result of mounting losses at the UAE national carrier. There is the potential for further rationalisation post-COVID.

Annual seat capacity operated by Emirates, Etihad & Qatar Airways, 2012-2022

Source: CAPA Advisory research and analysis; OAG

Whether Etihad and Emirates will eventually merge has been the subject of speculation for many years but there is nothing to suggest that this is imminent. Either way, Etihad’s decision to follow a more strategic path rather than being focused on growth will be beneficial for Emirates in terms of its network expansion and pricing power.

Going forward therefore, Emirates is expected to further entrench its position as the UAE’s dominant full service carrier with a fleet size (250+ aircraft) and an order book (close to 200 aircraft) around three times that of Etihad.

However, competition in the region will remain intense as a result of Qatar Airways’ ambitious plans and a potential new contender from Saudi Arabia to join the ME3.

Although Emirates may face a reduced threat from its immediate neighbour in Abu Dhabi, Qatar Airways has no plans to slowdown. The Doha-based carrier remained very active through the pandemic. In fact, it reduced its operations by a lesser proportion than just about any other carrier, including Emirates, and is recovering quickly. The carrier will be further buoyed by the traffic and brand visibility that will result from Qatar hosting the FIFA World Cup 2022 at the end of this year.

But if Emirates and Qatar Airways were under the impression that Etihad’s more conservative plans would enable them to emerge as the undisputed ME2, Saudi Arabia has other ideas.

As Saudi Arabia seeks to transition from its traditional dependence on oil, tourism has been identified as one of the priority pillars of the new economy, with a target of attracting 100 million visitors by 2030. This is an ambitious target for any country, but especially for one that only formally opened its doors to leisure tourism in 2019.

Billions of dollars are being invested in destinations and infrastructure (e.g. Red Sea resorts, golf courses, a raft of high end properties in Al Ula which have received extensive coverage in global travel publications,) and events (including concerts and festivals) intended to project a new image of Saudi Arabia, although a number of sensitive issues remain.

Connectivity will be fundamental to achieving the tourism targets. For that reason, Saudi Arabia has announced plans to launch a new airline that will offer a product that is intended to be more appealing to foreign visitors and to transfer passengers (enabling the developing of a global hub in Riyadh), leaving Saudia to focus on religious traffic and other market segments.

There is no question that the government has the capital to develop a new world class airline, designed on the model of Emirates. However, expertise and execution will be critical and there are various hurdles that remain to be overcome. And it will take time. It is unlikely that the new carrier could be considered a genuine candidate for membership of the New ME3 until the 2030s or beyond. But it is feasible to expect that Emirates will face increased competition in its neighbourhood.

Competition is also likely to increase from the east as a new Air India emerges post-privatisation.

India has historically been a quasi-home market for Emirates. In 2019 the carrier deployed almost 9% of its global seat capacity in India, the highest share of any country in the world. And with around two-thirds of those seats being used for sixth freedom traffic, the India routes support a significant proportion of Emirates’ capacity to North America, Europe and even the Middle East.

Emirates is the largest foreign carrier in India and has been able to achieve this position because of the historical weakness and limited size of India’s full service carriers. But the state-owned national carrier, Air India was recently privatised and handed over to Tata Sons, one of India’s largest and most respected industrial conglomerates in Jan-2022.

The new owners are expected to invest in transforming Air India into a world class network carrier, seeking to claw back traffic that has been ceded to foreign airlines, by offering non-stop services to key markets with a highly competitive product.

Emirates may face increasing resistance in securing increased market access during future air service agreement negotiations.

During the pandemic governments around the world have extended up to USD200 billion of financial support to carriers, much of which may have to be written off. This could trigger a more protectionist approach in order to ringfence airlines from competition from super-connectors. After having invested such significant capital in bailing out their carriers, foreign governments may not be in a rush to liberalise access for airlines such as Emirates.

The gradual exit of A380s will have long-term implications for Emirates and the Dubai hub.

The A380 appears to have been an aircraft that was clearly far more suited to one airline than any other. Of the 251 A380s ordered, 123 were delivered to Emirates. The powerful Dubai hub enabled Emirates to consolidate traffic on a scale that other carriers could not match, for which the world’s largest commercial aircraft was ideal.

With 615 seats, the highest density version of the A380 that Emirates operates has almost 50% more seats that its largest 777, enabling it to maximise traffic at slot-constrained airports.

The suspension of the A380 programme and the gradual phasing out of the aircraft will result in the loss of a significant competitive advantage for the carrier, providing competitors with a more level playing field. There are no signs of a replacement very large aircraft, despite Emirates urging OEMs to consider this.

As a result, a new network strategy will emerge for Emirates around the A350 and the 777X, although both programmes are currently facing various challenges. But with the reduced size of these aircraft types, Emirates will require more aircraft and frequencies to maintain capacity.

FlyDubai is expected to play a more strategic role as a complement to Emirates.

Although Emirates and FlyDubai are independent carriers, their common ownership means that there is an opportunity for them to engage in closer cooperation in terms of network integration, codesharing and schedule coordination than they have already been pursuing.

Emirates and FlyDubai are expected to remain distinct brands, but the two carriers will likely increasingly work together like a single group.

FlyDubai is expected to play an increasing role in terms of opening up secondary cities across the Middle East, North & East Africa, Central Asia, South Asia and even parts of Southeast Asia where the volume and yield may not be appropriate for widebody or full service operations, but there nevertheless exists OD and sixth freedom demand that can add value at a group level.

Emirates will need to prepare for a new era post-Tim Clark

Under the leadership of Sir Tim Clark – and Sir Maurice Flanagan before him – Emirates has emerged as a world class airline in terms of scale, service and strategic impact. It is one of the aviation industry’s most enduring success stories.

Emirates has been fortunate to have at its helm a President who has been with the airline since it was founded almost 40 years ago. But Sir Tim has indicated that he will be stepping down shortly (and would already have done so if not for the pandemic).

As Emirates prepares for a new leader to step in, during what is a very challenging external environment, the carrier will need somebody that is not only able to maintain the network, hub and product strengths that are hallmarks of the airline, but is able to simultaneously position Emirates to become a digital and an environmentally sustainable carrier.

Key learning: Successful airlines constantly innovate to influence change rather than be dictated by it.

During the pandemic Emirates has demonstrated that despite its size and scale it is focused on proactively addressing challenges by continuously investing in people, products and processes. With a proposed IPO, implementation of NDC, a continued emphasis on training and greater adoption of digitalisation, Emirates has the strategic determination to remain a market leader.

Complacency can be the downfall of successful airlines. Emirates has not sat back but has focused on constant innovation and constant renewal to remain ahead of industry developments.

This approach should position the airline well to navigate the challenges ahead, ranging from increased competition in the Gulf region and India, the prospect of market access challenges in countries beyond and the need to restructure the fleet plan around the phasing out of the A380 and the induction of a larger number of A350s/777Xs. As a result, a new Emirates should emerge in the coming years.